As the baby-boomer generation starts to retire and younger families are having fewer children, Social Security will face significant challenges in maintaining financial stability and providing expected benefits to future retirees.

Data

Forecasting

Economy

JobsEQ

Analysis

Consulting

Plus

Pro

Economic Trends

As the baby-boomer generation starts to retire and younger families are having fewer children, Social Security will face significant challenges in maintaining financial stability and providing expected benefits to future retirees. The program’s pay-as-you-go design, where retirement benefits for one generation are not paid by their own contributions, but that of following generations, raises solvency concerns in light of demographic patterns. American workers recognize the danger - a Transamerica Institute survey reported 72% of working Americans fear Social Security won’t be there for them when they retire.[1] Current projections, however, show the program will have funding for decades to come, but may not be able to pay as much as scheduled - the amount largely depends on shifting demographics and future program changes.

Changes from the Historical Promise of Social Security

Social Security was never designed to be a comprehensive retirement plan, but to be a safety net for retirees. The program started in 1935 to provide a guaranteed income in retirement and protect senior citizens against the risk of outliving their savings. It now provides income security to more than 65 million Americans who are retired, disabled, or have experienced the death of a working spouse or parent. In fact, Social Security benefits play an essential part in reducing poverty and lifts more people above the poverty line than any other government program.[2] Without the program, an estimated 21.7 million more people would live below the poverty line (based on a March 2022 analysis).[3]

By 2035, workers entering retirement may not receive as much as planned. The pay-as-you-go program, where current workers’ payroll taxes fund benefits to current beneficiaries, is projected to only cover 80% of scheduled benefits in 2035, according to the Social Security Administration (SSA).[4]

The Future of Social Security

As the gap between outlays and revenues widens, existing and incoming funds will struggle to support the financial stability of the program. Already in 2010, annual outlays exceeded annual revenues for the first time (accounting for interest). Since then, the gap between outlays and revenues has persisted, with outlays exceeding tax revenues by almost 9% in 2015.[5} Currently, shortfalls are funded by the program’s two trust funds (jointly known as the Old-Age, Survivors, Disability Insurance or OASDI), which are sufficient to support full scheduled benefits until 2034.[6] Afterwards, the SSA projects the expanding gap will result in a 20% deficiency of benefits paid after 2034.[7] The Congressional Budget Office (CBO) projects a more substantial decrease, with benefits expected to be 25% smaller in 2034.[8]

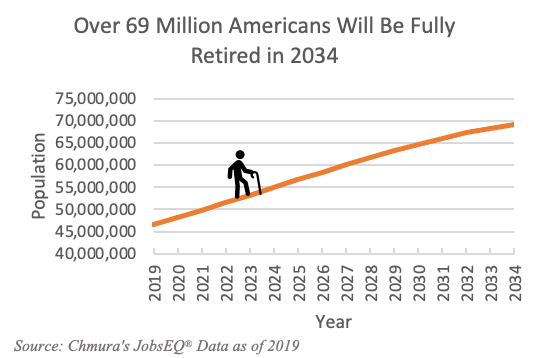

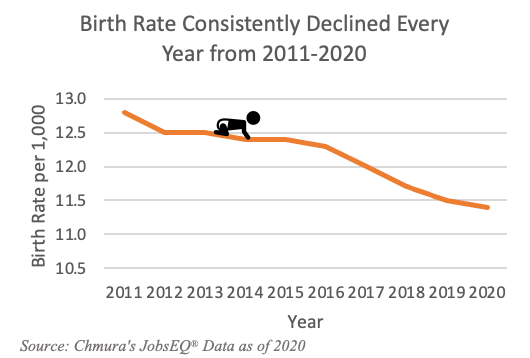

Current demographic trends raise further concerns about Social Security’s benefits. To investigate the role of demographics, the Data Explorer feature of Chmura’s JobsEQ® was used to produce birth rate trends and population projections. The number of Americans 67 (full retirement age) and older is projected to increase from 46.6 million to over 69 million from 2019 to 2034, due to higher life expectancy and the aging baby-boom population.[9] At the same time, birth rates have consistently declined every year from 2011 to 2020, meaning there will be fewer workers contributing to future retiree benefits. As a result of more retired workers, people living longer, and declining birth rates, the SSA projects that the current ratio of 2.8 workers paying Social Security taxes to each person collecting benefits will fall to 2.3 by 2038. [10] In short, younger generations can expect to receive fewer benefits for the same amount paid into Social Security while working; but should not expect to receive zero Social Security benefits in retirement, if there is no change to the current social security system.

To address these concerns, the CBO outlined possible solutions that will allow the program to be sustainable until 2097. If If the SSA were to pay fully scheduled benefits, the CBO predicts spending on the program would increase from 5.2% of GDP in 2023 to 7.0% in 2097. [11] To fund this, the federal government could raise payroll taxes immediately and permanently by 5.1 percentage points (currently 12.4%). Alternatively, reducing scheduled benefits by an amount equivalent to 5.1% of taxable payroll, or combining tax increases with benefit reductions, would make the program sustainable until 2097. Notably, balancing the budget will not be enough to keep the program sustainable at current levels - these proposed policies would create annual surpluses over the next three decades to offset projected deficits until 2097. Moreover, Congress may consider raising the full retirement age to delay benefit payouts and slow growing costs, with results varying based on how fast and high it’s raised.[12]

If no changes are made, Social Security will not be able to fully pay scheduled benefits in the next decade and workers will need to fill future retirement gaps. Kathy Indiano, a Social Security accountant, explains the program was designed to be a piece of the retirement pie, not an exhaustive retirement plan.[13] With the possibility of each progressing generation getting less than the last, individuals will need to plan ahead and adjust accordingly. Creating early financial plans, investing early to benefit from compounding, and saving in tax-incentivized retirement accounts (i.e., 401ks, IRAs) are some viable solutions for individuals to fill future gaps.

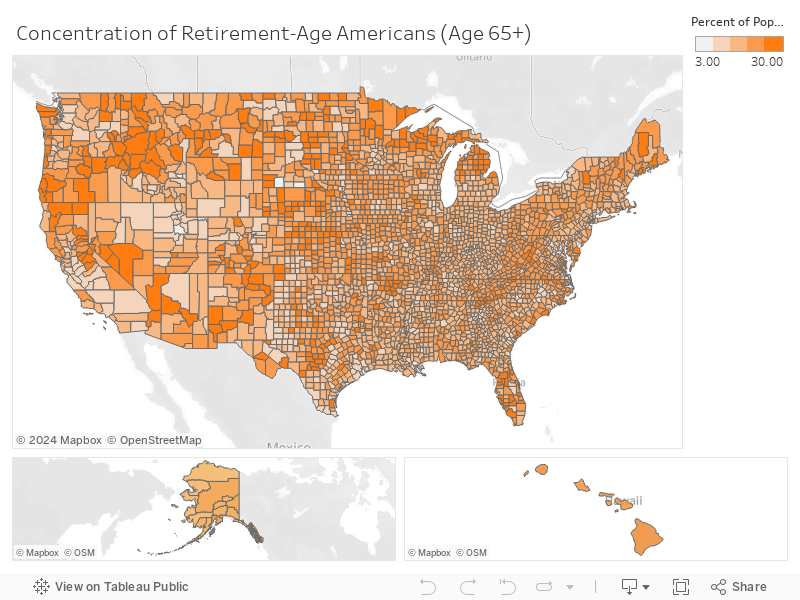

Localities will also need to evaluate the implications of increasing retirements and plan ahead. In the coming decade, counties with a high concentration of retirement-age workers (2021 data shown in the map below) may experience a shrinking labor force, impacting skill availability and economic productivity in the area.[14] These counties may consider investing in training programs to ensure institutional knowledge is passed to younger workers, attracting young skilled workers, and/or incentivizing workers to delay retirement.

As Social Security benefits decrease, localities with a larger share of retirees may also expect a reduction in spending and possibly slower GDP growth, as those with fixed income from Social Security checks tend to have fixed levels of spending on retail and entertainment.[15] Conversely, counties that provide desirable retirement environments, including access to healthcare, amenities, and a lower cost of living may attract retirees who seek to maximize their Social Security benefits. The future influx of retirees may also have positive economic implications including increased demand for housing, healthcare workers, and local businesses catering to seniors.[16]

To further explore how JobsEQ® can be used to evaluate demographic trends and impacts from the national level down to your zip code, contact Chmura today.

--------------------------------------------

[1] Source: https://transamericainstitute.org/docs/default-source/research/stepping-into-the-future-employers-workers-multigenerational-workforce-report.pdf

[2] Source: https://www.cbpp.org/blog/social-security-is-not-bankrupt

[3] Source: https://www.cbpp.org/research/social-security/social-security-lifts-more-people-above-the-poverty-line-than-any-other

[4] Source: https://www.ssa.gov/oact/TRSUM/index.html

[5] Source: https://www.cbo.gov/publication/51011

[6] Source: https://www.aarp.org/retirement/social-security/questions-answers/how-much-longer-will-social-security-be-around.html

[7] Source: https://www.ssa.gov/oact/TRSUM/index.html

[8] Source: https://www.cbo.gov/system/files/2023-06/59184-SocialSecurity.pdf

[9] Source: https://www.urban.org/policy-centers/cross-center-initiatives/program-retirement-policy/projects/data-warehouse/what-future-holds/us-population-aging

[10] Source: https://www.ssa.gov/news/press/factsheets/basicfact-alt.pdf

[11] Source: https://www.cbo.gov/system/files/2023-06/59184-SocialSecurity.pdf

[12] Source: https://www.actuary.org/node/13799

[13] Source: https://www.nytimes.com/2022/10/14/business/social-security-millennials-baby-boomers.html

[14] Source: https://www.glensfalls.com/glensfallsbusinessjournal/2021/06/skilled-trade-labor-shortages-continue-as-boomers-retire-replacements-arent-there/

[15] Source: https://www.jpmorganchase.com/institute/research/cities-local-communities/insight-spend-by-seniors

[16] Source: https://www.jpmorganchase.com/institute/research/cities-local-communities/insight-spend-by-seniors