The U.S. economy has entered its longest expansionary period in history. Theoretically, inflation should be rising, but it’s not. Theoretical...

By Mike Chmura

Published Jul 15, 2019

The U.S. economy has entered its longest expansionary period in history. Theoretically, inflation should be rising, but it’s not. Theoretical macroeconomic thought about inflation and unemployment is often guided by the Phillip’s Curve, an economic theory which postulates an inverse relationship between unemployment and inflation rates on a macro-level. For example, a lower unemployment rate would correspond to a higher inflation rate because the labor supply would be limited when the unemployment rate falls around or below its level of full employment. Thus, the restricted labor supply would encourage employers to raise wages to attract qualified employees. This would, in turn, lead to a rise in inflation as wages are an important component of the costs of products and services. Since its conception in 1958, the Phillip’s Curve has been the subject of many arguments over its assumptions and applications because this inverse relationship doesn’t always hold true when analyzing real-world data. The current expansion is a good example.

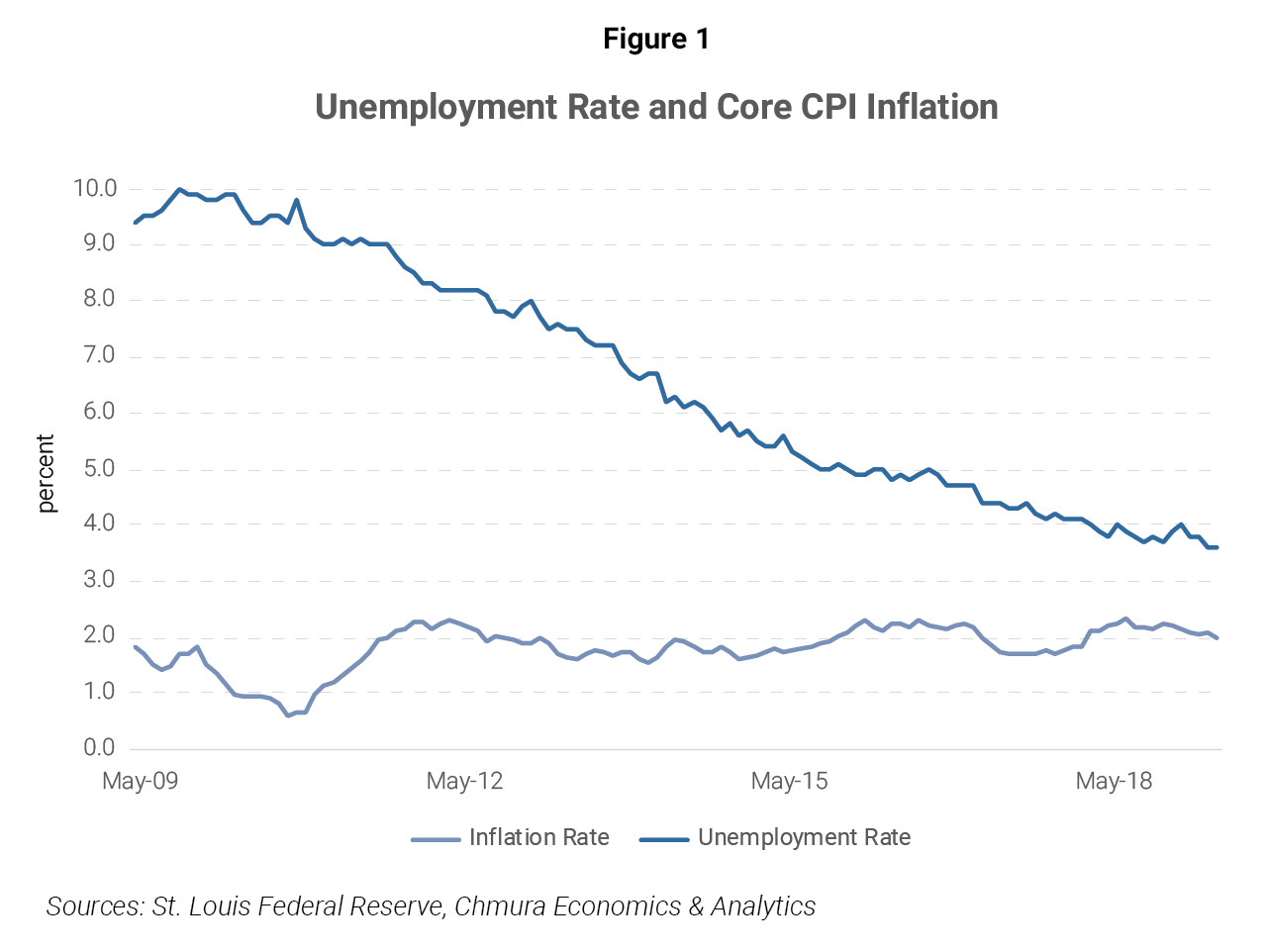

As of July 1, 2019, the United States entered its longest economic expansionary period in history, and according to macroeconomic theory (the Phillip’s Curve, in particular), inflation should be increasing. However, inflation rates, based on the core consumer price index (CPI),[1] (see Figure 1) have remained relatively stable around 2% since the beginning of the expansion, even decreasing noticeably in some months.

So, inflation is remaining low even though the unemployment rate has decreased to a low not seen since 1969. Why is this happening and what are the current changes to market forces and/or demographics that are causing inflation to remain low despite the tight labor market?

The overall price level can be influenced by several factors. Increasing wages and the cost of supplies certainly play important roles in the prices of goods and services. In addition, inflation expectations may also affect prices faced by consumers.

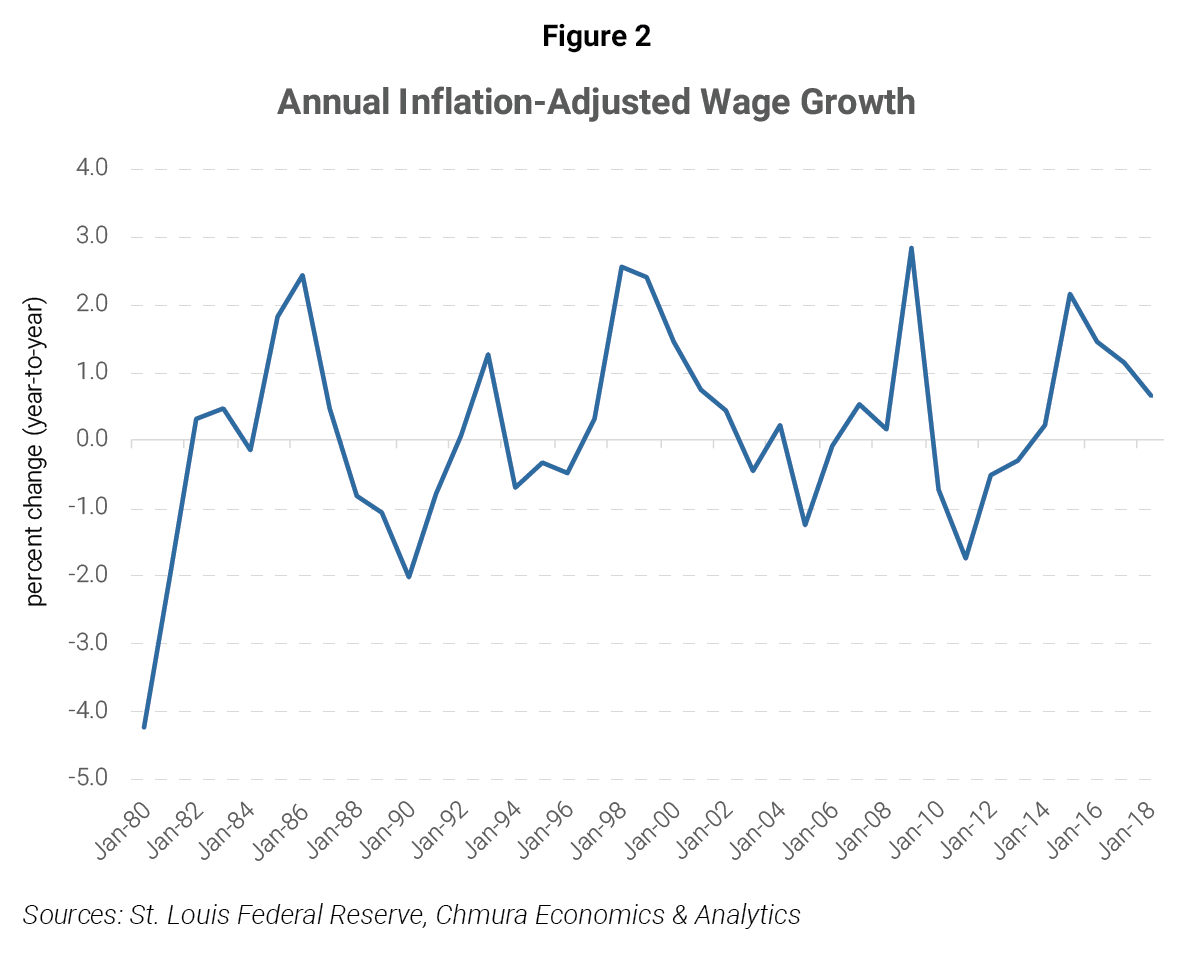

Analyzing current wage growth data to see if wages are increasing like the Phillip’s Curve relationship would suggest, we find that there was an increase in wages since the nation entered its current expansion. Recently, however, real wage growth has slowed, averaging only 0.6% for 2018. (see Figure 2). Real wage growth may indeed lead to increased inflation, but recently wages have only increased at a modest pace. Nevertheless, any wage growth, no matter how small, has the ability to affect inflation rates.

Wage increases can certainly cause inflation to rise; nonetheless, they may not translate into price increases faced by consumers because businesses could cut costs elsewhere, improve productivity, or absorb the wage increases. The CPI, commonly used to measure inflation, utilizes a basket of consumer goods to track overall price level variations. If the costs of production for certain goods and/or services have decreased, then the pace of inflation may slow. CPI data from the Bureau of Labor Statistics (BLS) show that prices for apparel, medical care commodities, and new vehicles have experienced periods of decline in average price over the past two years.[2] Lower prices in these industries may have offset some other price increases for housing and medical care services.

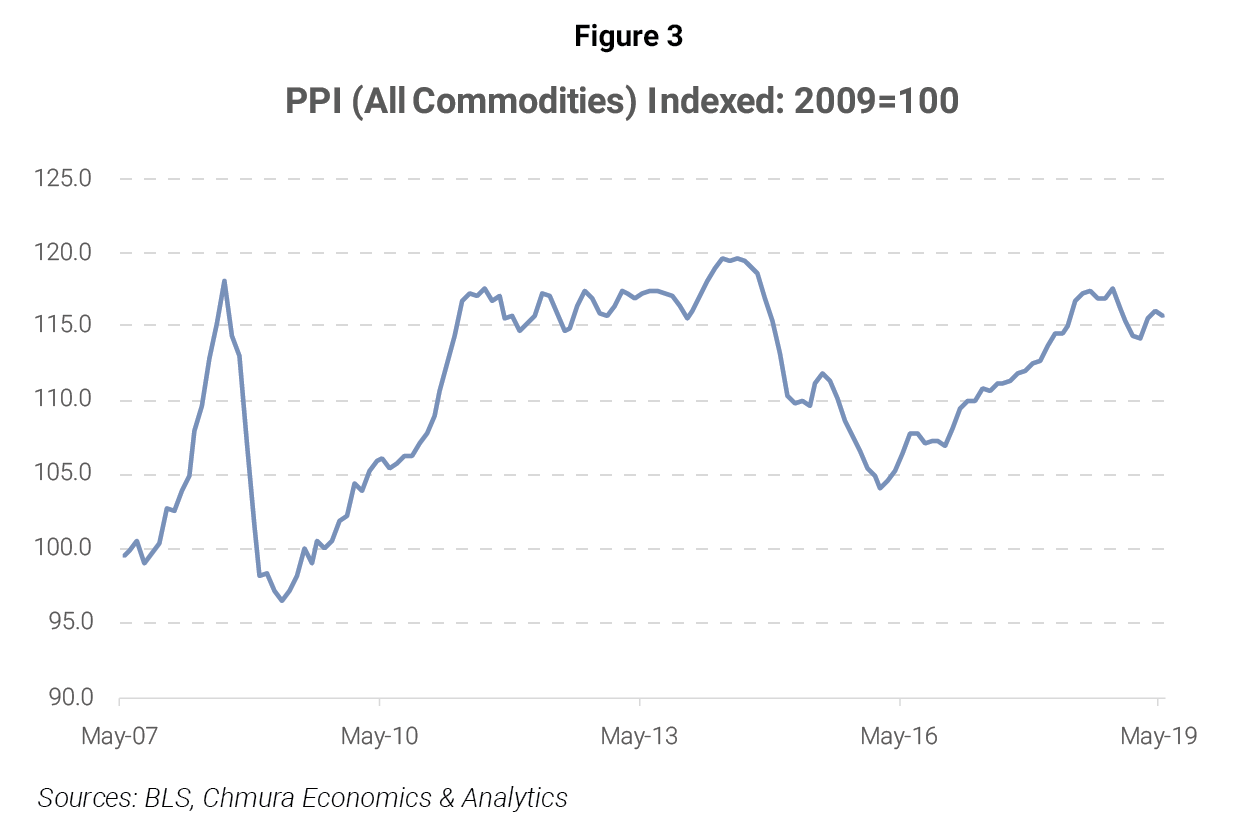

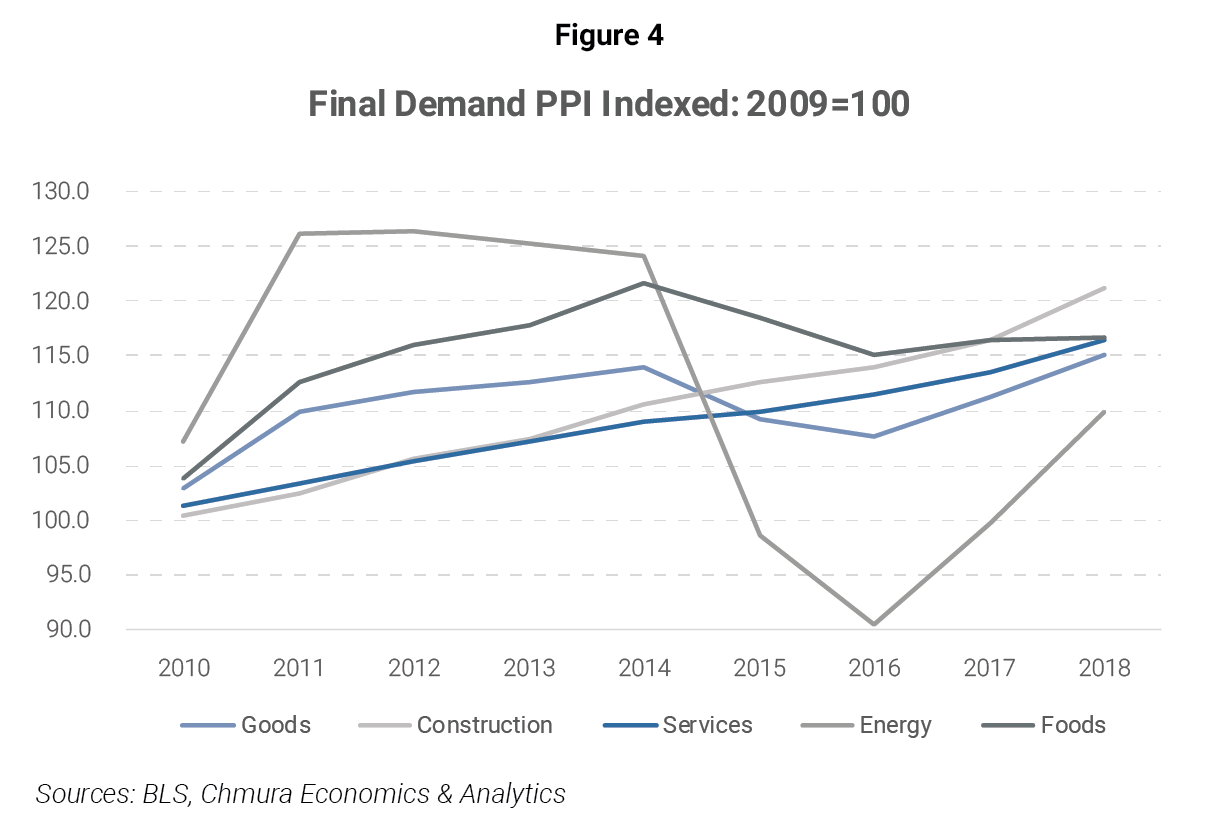

Furthermore, producer price index (PPI) data may provide insight into why inflation is remaining low. The PPI is similar to the CPI, but it measures costs faced by producers, not the selling price (cost to the consumer). As seen in Figure 3 (above), PPI has been generally increasing since the end of the Great Recession, with one period of decline starting in 2014 and ending in 2016. Breaking the PPI data down into different final demand commodity types (Figure 4), we see energy, foods, and goods production costs dropped from 2014 through 2016. The overall PPI drop during the same period was primarily due to the price decrease for these same commodities. However, for the most part, prices for producers have been increasing since the Great Recession. Interestingly, the drop in producer costs for energy, foods, and goods coincided with a period of high wage growth—this decrease in PPI likely kept inflation steady despite the rapid wage increase. Although there is clearly an increase in the PPI, averaging 1.2% annual growth since 2010, it is possible that this increase is small enough as to not cause inflation to increase much faster than 2%.

The pace of inflation is also influenced by people’s expectations about future inflation. If individuals believe prices will rise, then they will factor price changes into wage contracts, product pricing, etc. Worse, if people come to expect persistently large increases in inflation, then these expectations will only add momentum to inflation as people buy products before prices rise further, causing supply shortages and more price increases. This is what makes inflation erratic in some cases and rise even if production-side costs are generally deceasing or not increasing as fast as inflation.[3]

The best defense against potentially harmful inflation expectations is maintaining a stable expected inflation rate. This task falls to the Federal Reserve in the United States. The Federal Reserve has targeted a 2% annual inflation rate along with its dual mandate of maximum employment.[4] Jerome Powell, the current chairman of the Federal Reserve, credited smarter Federal Reserve monetary policy for why inflation has recently remained stable despite the labor market tightening (i.e. unemployment decreasing). In his address at the 60th Annual Meeting of the National Association for Business Economics, Powell discussed this topic at length saying, “When monetary policy tends to offset shocks to inflation,… a surprise rise or fall in labor market tightness will naturally have smaller and less persistent effects on inflation.”[5] The Federal Reserve’s inflation targeting practice has likely helped to keep inflation rates low.

Additionally, there exist aspects to inflation which economists either do not currently comprehend or cannot quantify. Powell admitted as much saying, “we do not fully understand the causes and implications of [inflation].”[6] Nonetheless, if the Federal Reserve continues to abide by proper “risk management” practices, possible future increases to inflation resulting from tight labor markets will likely not have a catastrophic impact.

Overall, there seems to be no single factor that has helped maintain the low inflation rate. Instead, the inflation rate has likely been affected by multiple factors. A combination of accurate inflation targeting policy by the Federal Reserve and different changes in wages and production costs have all contributed to the recent inflation rate. In the period right after the Great Recession, when production costs increased, there was enough slack on the labor market to prevent wage growth. In recent years, while the labor market tightened, we were fortunate to have lower production-side costs for certain commodities (e.g., energy).

Economists are not all in consensus on if low inflation rates can be maintained while the unemployment rate continues to decrease. There is still much uncertainty over recent events which could impact the economy. Tensions with Iran have already caused oil prices to rise,[7] and this may continue if relations between Iran and Western Powers do not improve. Also, President Trump’s tariffs (especially those against China) may begin to be felt by producers, hence driving up prices.

Ultimately, no matter the cause, the current thriving economy with low inflation and unemployment is benefiting many Americans. Potential risks certainly still lurk with this combination, but currently the vast majority of the effects are positive—that’s something not often experienced.

[1] The core CPI excludes food and energy prices which tend to be volatile.

[2] Data can be found here: https://www.bls.gov/charts/consumer-price-index/consumer-price-index-by-category-line-chart.htm

[3] This phenomenon can also work in reverse, leading to deflation.

[4] Maximum employment refers to a state of equilibrium unemployment, also known as the “Natural Rate of Unemployment.”

[5] Chair Powell’s full speech can be read here: https://www.federalreserve.gov/newsevents/speech/powell20181002a.htm

[6] Ibid.

[7] Source: https://www.cnbc.com/2019/06/24/asia-markets-us-iran-oil-and-currencies-in-focus.html