Talk of recession has picked up again. The reason might sound complicated, but the principle is fairly basic. In financial parlance, we’re...

By Chris Chmura

Published Apr 8, 2019

Talk of recession has picked up again. The reason might sound complicated, but the principle is fairly basic.

In financial parlance, we’re talking about the inversion of the yield curve. Here’s what that means … and how it might take a bit of time to know the consequences.

The U.S. Treasury Department sells government bonds at various maturity dates — ranging from one month to 30 years — and it pays interest on that money it is borrowing. The “yield curve” simply represents the relationship between interest rates on short-term and longer-term securities.

Typically, the yield on a three-month Treasury bill is lower than on a 10-year note. That’s because there is lower uncertainty over what will happen in only three months.

For example, the holders of a 10-year note have a longer period to worry about the economy. If inflation goes from 2 to 3 percent in that decade, they will have less purchasing power when the note matures. To compensate for that risk, they demand a higher interest rate.

So the yield curve typically shows incremental increases between the three-month bill, the one-year bill … and so on, up to 30-year Treasuries.

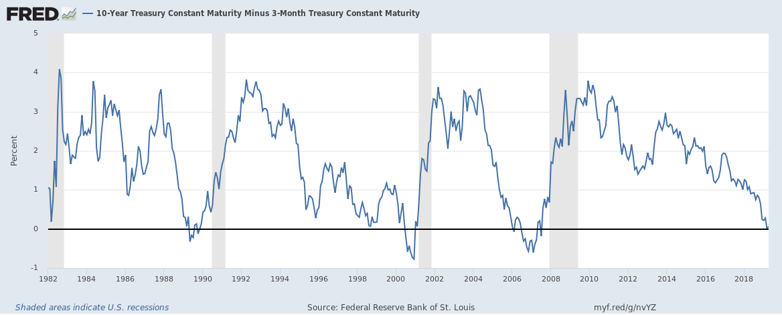

But the curve is said to invert when the three-month yield is higher than the 10-year yield. When that happens, it indicates that investors have concern about economic growth.

For the inversion to happen, two things need to occur. One is that short-term interest rates have to rise, and the other is that long-term rates have to stay put or decline.

Here’s what has been happening lately.

The goal of the Federal Reserve Board is to bring short-term rates to a level where they don’t cause the economy to accelerate so much that inflation rises.

For two years, the Fed has been raising the federal funds rate target — the overnight rate that banks use to lend money to each other. The yield on the three-month bill rises almost in lockstep.

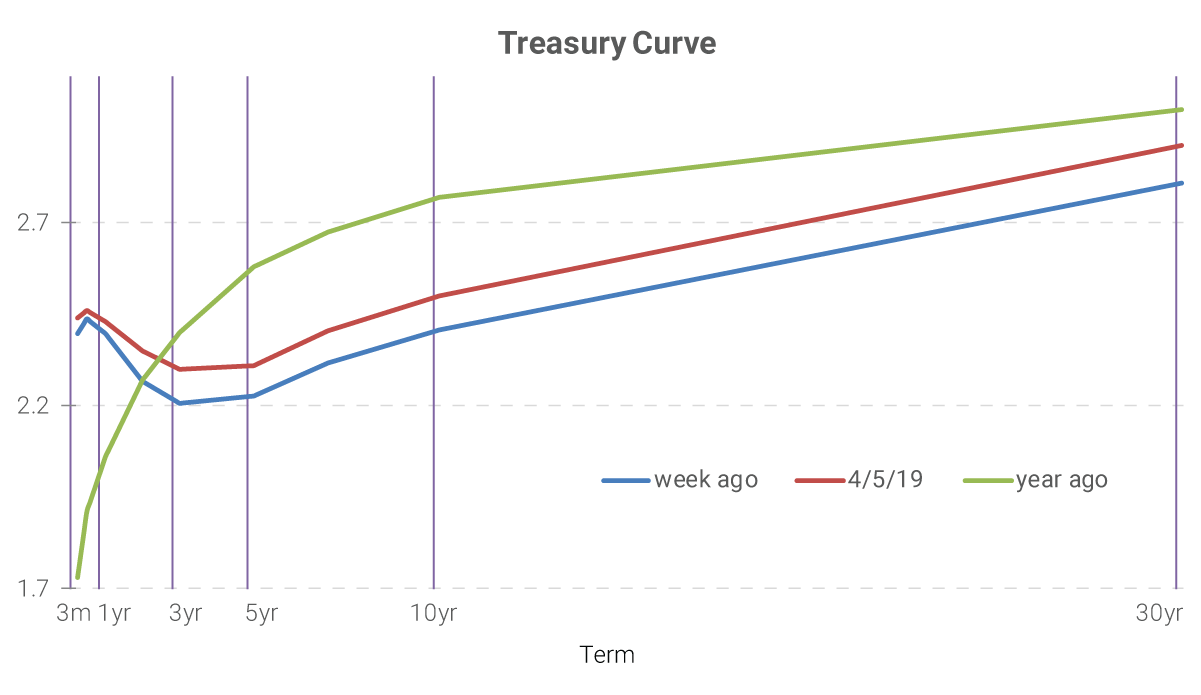

The Fed has raised the fed funds rate target to a range of 2.25 to 2.5 percent. That pushed the three-month yield to 2.46 percent for the week ending March 22, while the 10-year yield closed the week at 2.44 percent. (The March 29 closing yields were not quite inverted, with the three-month figure at 2.40 percent and the 10-year at 2.41 percent.)

Typically, when short-term rates rise, so do long-term rates. But this has not happened lately — because investors are concerned that economic growth will slow. That would mean lower yields in the future.

So what do investors do? They buy more long-term Treasuries now to lock in current higher yields. The increased demand for long-term notes causes the price to go up, and the yield comes down — because Treasury prices and yields move in opposite directions. When this process pushes long-term interest rates below short-term rates, it results in yield curve inversion.

Since 1956, an inverted yield curve has preceded every recession by a year and a half or so. We’ll know before long whether today’s bond investors are right this time.